Quantitative Easing & the Nightmare It Has Created

Posted on October 23, 2015 by Martin Armstrong

While so many people claimed that Quantitative Easing (QE) would produce inflation since it was the creation of money, the truth is very far from this simplistic idea. The theory used by the central banks is seriously flawed and a throwback to ancient times before 1971. There used to be a difference between debt and cash where you could not use debt as cash to borrow on. Then it was less inflationary to borrow than to print, but that changed post-1971. If you want to trade today, you post T-bills as cash. The REPO market has emerged where AAA securities can be borrowed against for the night.

Therefore, buying in bonds to inject cash into the system under the old way of running the monetary system pre-1971 made sense. Today, it is proving to be a fool’s game. Why? This is merely swapping debt for cash; the REAL money supply has not increased when the true definition of the base in money supply is debt + cash. Then you add the leverage from banking.

So what does this new reality mean? Under QE, the central banks are the bidders supporting the market in the same stupid manner as attempting to peg a currency. The ECB under Draghai has lost its mind. They keep increasing the percentage of bonds they buy in hopes of creating inflation, but nothing is working. The bonds will not crash without a free market, but instead, they could become extinct. In order for a crash to materialize, there has to be a free market where the private sector bids. But what happens when the private sector has no interest? Oops! Extinction.

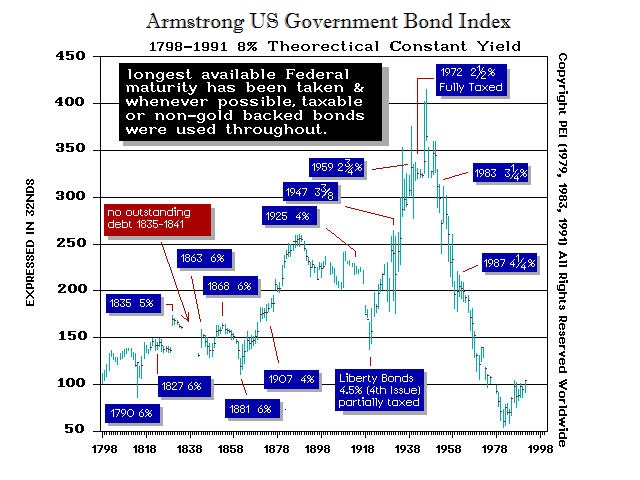

Little known to most analysts, during World War II, Congress ordered the Federal Reserve to do something similar to QE. The declared that the Fed MUST support the bond market during the war and be the constant buyer at PAR. The market went sideways during the war and what we see is a flat line. The Fed did not buy in the debt, it was just at a fixed bid.

Little known to most analysts, during World War II, Congress ordered the Federal Reserve to do something similar to QE. The declared that the Fed MUST support the bond market during the war and be the constant buyer at PAR. The market went sideways during the war and what we see is a flat line. The Fed did not buy in the debt, it was just at a fixed bid.

In the case of the central bank artificially supporting the bond market during World War II, that decree was lifted in 1951. Our present situation is different insofar as the central banks have bought all the long-term debt so there is a shortage of debt in the short-term. This is also why the Fed is accommodating the banks paying 0.25% on excess reserves.

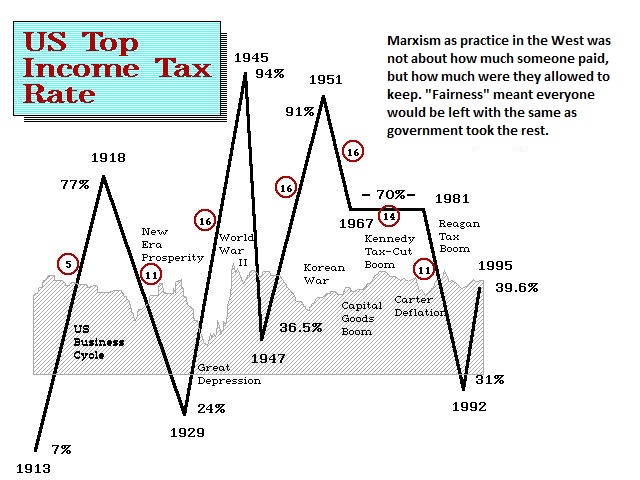

They are trying to figure out this Rubik Cube mess that they have created by cunning and stalking the financial market like a cat. The truth is rather scary. The rise in taxation is destroying the economy. Ancient Egypt was perhaps the most heavily taxed nation in history, and that was the primary reason it collapsed under the weight of the levies imposed on the populace that destroyed the economy by weakening the nation from the inside out.

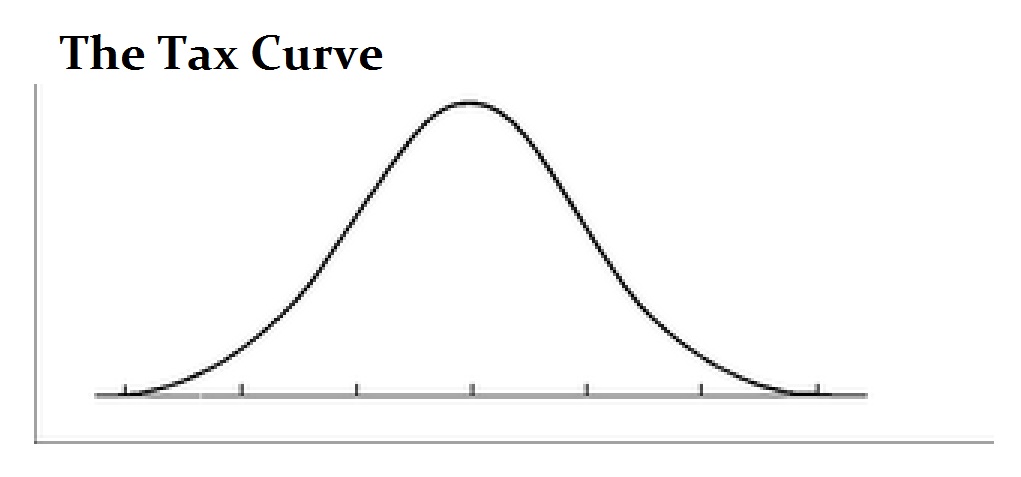

Unlike 1951, we are now at the extreme in economic destruction by the state in their hunt for taxes. Payroll taxes were introduced for the war; it was postwar when taxes were reduced in 1951 and the economy began to take off. We are exactly on the opposite side of the curve with rising taxes. This warns that we are on the collapsing side of the bell curve.

It is like alcohol. A little is good and too much kills you. Studies have shown that people who drink a little are healthier than those who drink too much or none at all. This time, with taxes rising, there is a contracting global economy and we are in serious trouble. The central banks have bought in the debt rather than declaring they will support the market. This means that they will not have a market to reverse the position and sell the debt they bought in. This means that a sovereign default wipes out central banks as well. Hence, the long-end of the market is being systematically rendered extinct.

We may see the bonds crash in price to the extent that people are not interested. However, the central banks will have to buy in more and more debt. This raises the risk of “conversione forzosa”, whereby even if you bought 30-day government paper, they simply decree that they will not repay that obligation for 10 years. They can simply convert short-term to long-term. We are more likely to see this type of action before any real reform.

This entry was posted in The Global Market and tagged Central Banks, conversione forzosa, Quantitative Easing, tax curve by Martin Armstrong. Bookmark the permalink.

Posted on October 23, 2015 by Martin Armstrong

While so many people claimed that Quantitative Easing (QE) would produce inflation since it was the creation of money, the truth is very far from this simplistic idea. The theory used by the central banks is seriously flawed and a throwback to ancient times before 1971. There used to be a difference between debt and cash where you could not use debt as cash to borrow on. Then it was less inflationary to borrow than to print, but that changed post-1971. If you want to trade today, you post T-bills as cash. The REPO market has emerged where AAA securities can be borrowed against for the night.

Therefore, buying in bonds to inject cash into the system under the old way of running the monetary system pre-1971 made sense. Today, it is proving to be a fool’s game. Why? This is merely swapping debt for cash; the REAL money supply has not increased when the true definition of the base in money supply is debt + cash. Then you add the leverage from banking.

So what does this new reality mean? Under QE, the central banks are the bidders supporting the market in the same stupid manner as attempting to peg a currency. The ECB under Draghai has lost its mind. They keep increasing the percentage of bonds they buy in hopes of creating inflation, but nothing is working. The bonds will not crash without a free market, but instead, they could become extinct. In order for a crash to materialize, there has to be a free market where the private sector bids. But what happens when the private sector has no interest? Oops! Extinction.

In the case of the central bank artificially supporting the bond market during World War II, that decree was lifted in 1951. Our present situation is different insofar as the central banks have bought all the long-term debt so there is a shortage of debt in the short-term. This is also why the Fed is accommodating the banks paying 0.25% on excess reserves.

They are trying to figure out this Rubik Cube mess that they have created by cunning and stalking the financial market like a cat. The truth is rather scary. The rise in taxation is destroying the economy. Ancient Egypt was perhaps the most heavily taxed nation in history, and that was the primary reason it collapsed under the weight of the levies imposed on the populace that destroyed the economy by weakening the nation from the inside out.

Unlike 1951, we are now at the extreme in economic destruction by the state in their hunt for taxes. Payroll taxes were introduced for the war; it was postwar when taxes were reduced in 1951 and the economy began to take off. We are exactly on the opposite side of the curve with rising taxes. This warns that we are on the collapsing side of the bell curve.

It is like alcohol. A little is good and too much kills you. Studies have shown that people who drink a little are healthier than those who drink too much or none at all. This time, with taxes rising, there is a contracting global economy and we are in serious trouble. The central banks have bought in the debt rather than declaring they will support the market. This means that they will not have a market to reverse the position and sell the debt they bought in. This means that a sovereign default wipes out central banks as well. Hence, the long-end of the market is being systematically rendered extinct.

We may see the bonds crash in price to the extent that people are not interested. However, the central banks will have to buy in more and more debt. This raises the risk of “conversione forzosa”, whereby even if you bought 30-day government paper, they simply decree that they will not repay that obligation for 10 years. They can simply convert short-term to long-term. We are more likely to see this type of action before any real reform.

This entry was posted in The Global Market and tagged Central Banks, conversione forzosa, Quantitative Easing, tax curve by Martin Armstrong. Bookmark the permalink.

» Al-Ardawi: The Sudanese government seeks to liberalize the Iraqi dinar and stabilize the economy

» utube 4/18/24 Iraq: Over 14 Agreements Signed Between Iraq and US BREAKING NEWS from Congress.

» utube MM&C 4/16/24 IQD Update - Iraq Dinar - America - Activate - Massive Economic Deals -

» utube MM&c 4/19/24 Iraqi Dinar - Private Sector - Economic Stability - Financial Reform - Al Sudan

» Iraq officially signs the “Singapore” agreement to resolve trade disputes

» Parliament Finance advises raising exchange rates again... What about oil revenues?

» Al-Sudani: Iraq is in the process of recovery and has taken its leading position that attracts work

» Al-Araji: Iraq is prepared to deal with all circumstances and seeks partnership with the United Stat

» Sudanese from Michigan: The government represents all components and is keen to take care of the aff

» Democratic Party: The "new generation" is the most corrupt and has dozens of cases in court

» What is the benefit of Iraq establishing a petrochemical plant in Egypt?!.. An oil expert explains

» A judicial delegation participates in the Permanent International Forum for Commercial Courts in Qat

» Al-Sudani: The government follows a balanced policy that makes Iraq a station for security

» Deduction of 160 million dinars from the salaries of MPs absent from Parliament sessions

» Central Bank: Washington praised Iraq's measures to resolve 80% of the financial transfer file

» Voices of Resilience: Al-Sudani’s frankness embarrasses the White House

» Al-Alaq confirms the formation of a committee between Baghdad and Washington regarding sanctions on

» Former MP: The Democrat will not hand over power after the regional elections

» Document/allocation of 20% of the lands of Al-Jawahiri Complex to employees of the Ministry of Defen

» Al-Hakim: Al-Sudani’s visit to Washington was a protocol and missed the two most important files

» Parliamentary Security: The National Security Service law will be voted on by Parliament soon

» Reconstruction and Housing: Zarbatieh residential project completed by 82%

» Al-Sudani reveals an intention to establish Al-Faw refinery with a capacity of 300 thousand barrels

» Government readiness to move the Doura refinery to an alternative location.. What are the conditions

» Al-Sudani’s visit to Washington.. Implications and results

» Association of Iraqi Private Banks: The suspension of some electronic payment services yesterday was

» Parliamentary memorandum.. Two solutions were before the Federal Court instead of removing the compo

» Blue fuel... Iraqi steps towards inexhaustible wealth for a century

» For fear of being "upset"... MPs "evade" signing to host Al-Sudani in Parliament

» Al-Sudani’s statement to convert 40% of Iraq’s exports into derivatives.. What does it have to do wi

» An Iraqi-American partnership to benefit from oil field gas

» The Minister of Commerce announces the distribution of the first payments of farmers’ dues for the 2

» Sudanese to members of the Iraqi community in the American city of Houston: Iraq has regained its he

» Romanski announces loans worth $50 million to support the Iraqi private sector

» Prime Minister: We plan to invest production capacities for export

» “Something happened” in Iran and no one is talking about Iraq and Syria. This is what we have so far

» Al-Sudani asks the American Baker Institute for assistance in preparing studies related to the oil m

» The Interior Ministry denies the occurrence of explosions inside Iraqi territory and diagnoses “the

» Tensions between Najaf and Baghdad over the airport... the rule of law over “military force” and the

» Al-Sudani from Washington: We agreed with Abu Dhabi on joint management of Al-Faw Port

» "Al-Party" talks about the region's elections and reveals the reason for refusing to pay salaries di

» Russia's oil is taking more of the Middle East's shares in the Indian market.. How much has Iraq los

» Early next month.. Traffic confirms that the electronic payment system is working only

» The Service Council accuses state departments of refraining from disbursing bonuses because of the m

» Electricity: The Baghdad street lighting campaign will be completed before the middle of this year

» Oil poses two conditions for moving the Doura refinery to an alternative location

» The Foreign Minister reveals the truth about his resignation and the reason for his departure to Erb

» Progress: Al-Halbousi’s acquittal has become conclusive, and his return to the presidency of Parliam

» Disagreements strike Al-Maliki's coalition over choosing the governor of Diyala

» The Union accuses Türkiye of exploiting the political situation for a ground incursion into Iraq

» The Democratic Party: Barzani is eagerly awaiting the results of Al-Sudani’s visit to Washington

» Frame: Al-Halbousi in the news and his return has become a pipe dream

» A parliamentary request to capitalize on Erdogan’s visit to Baghdad to end the water crisis

» Al-Sudani urges the US corporation Honeywell to help finish the Basra refinery

» Al-Sudani Meets with Representatives of Western Media Outlets in Washington

» Chairman of the Investment Authority signs the United Nations Convention on International Mediation

» PM: We will sign a contract to establish the Al-Faw refinery with a Chinese company

» PM arrives in Houston as part of his visit to USA

» Militia Man & Crew 4/18/24 Bush signed it and all presidents implemented it. Iraq’s funds have been

» Iraq is close to launching the electronic signature

» The Basra government discusses with an international oil company the implementation of social benefi

» The Prime Minister confirms to an American company: Gas projects in Iraq are a priority for the gove

» The Minister of Planning discusses with the World Bank mechanisms for scheduling external loans

» Oil sets the twenty-seventh of this month as the date for opening contracts for the fifth complement

» “Electronic begging”...professionalism and fabrication of stories” generates millions of dinars dail

» Al-Sudani calls on the American company Hanwell to contribute to the completion of the Basra refiner

» An American company expresses its willingness to establish LED lighting production lines in Iraq

» Including Iraq.. Iran announces the possibility of exporting 300 megawatts of “renewable electricity

» Political forces present two options to find an alternative to Al-Halbousi

» Parliament is awaiting the arrival of the budget schedules and the government is studying higher spe

» The International Monetary Fund adjusts its expectations for the development of the world’s economie

» A representative talks about the difficulty of finalizing the file of “electing the Speaker of Parli

» Work on preparing a law for diplomatic passports

» A female representative accuses the Ministry of Immigration of corruption

» Minister: Solving the Kurdistan salaries problem is the beginning of addressing other disputes betwe

» About 270 million dollars were sold by the Central Bank of Iraq in the currency auction

» The volume of trade exchange between Jordan and Iraq will exceed 800 million dinars in 2023

» Iraq signs memorandums of understanding with American companies in the fields of electricity, oil an

» The American company that manufactures the F16 expresses its readiness to implement the terms of con

» The volume of expected Qatari investments for the Iraq Fund for Development exceeds $3.5 billion

» Decrease in dollar prices in Baghdad and Erbil

» The President of the Region brings together the Kurdish parties to resolve the election file

» Al-Sudani receives in Washington the Chairman of JPMorgan

» Transport is starting to transform its ports into smart ones

» Sudanese reveals the volume of exchange with America

» "Al-Eqtisad News" publishes the memorandums of understanding signed between the Iraqi delegation and

» Al-Sudani urges an American company to contribute to establishing a chemical materials factory

» Iraq stresses the importance of Lockheed Martin's commitment to opening military aircraft maintenanc

» Iraq is on the verge of a “water disaster” by 2035

» Great satisfaction and optimism with the results of Sudanese’s visit to Washington

» Transport is beginning to adopt a plan to transform its ports into smart ones

» Completed 8,000 loan transactions at the Housing Bank

» Prime Minister: We plan to invest production capacities for export

» Transformation and partnership...a new horizon in Iraqi-American relations

» What is new in the economic dimension of the Washington visit?

» Two letters to the future

» National interests first

» Iraqi-American rapprochement...a national necessity