On the yearly level in Wheat CBT Futures, the last important low was established during 2010 at 4254, which was down 2 years from the high made back during 2008 at 13494. However, the highest closing was during 2007 at 8850. Right now, the market is trading below last year’s low of 4606. Overall, the market has been in a long-term bearish trend. At this time, the market is trading in a bearish position below our yearly momentum indicators warning resistance starts at 5990.

Honing in on the longer term yearly level, we see turning points where highs or lows on an intraday or closing basis should form will be, 2017, 2020, 2023 and 2025. Considering all factors, there is a possibility of a decline moving into 2017 with the opposite trend thereafter into 2020. This is a realistic potential since we have already penetrated last year’s low of 4606. The Yearly Bearish Reversal lies at 3110. Wheat has fallen to 3866 so far here in 2016. As long as 2016 holds 3110 for the year-end closing, then we should be looking a forming as early as 2017. We have already penetrated also the 2010 low of 4254.

Focusing an important timing model, the Directional Change Model target is 2017. This model often picks the high or low, but can also elect a breakout to a new higher trading zone or a breakdown to a new lower trading level.

YEARLY TECHNICAL ANALYSIS

01/01/2016… 2198 4523 5450 8460

01/01/2017… 2219 4656 4445 8510

01/01/2018… 2240 4790 3439 8560

01/01/2019… 2261 4923 2434 8610

01/01/2020… 2282 5056 1428 8660

01/01/2021… 2303 5190 423 8710

01/01/2022… 2325 5323 8760

YEARLY ANALYSIS

In the event of new intraday lows developing beyond this year, then the final low could extend into 2017. Broadly speaking, a month-end closing BELOW 3070 is where the critical support lies. Only a monthly closing BELOW 3070 will confirm a long-term bear market is in motion. Otherwise, here lies important dynamic support within this market and holding this level is a clear line of demarcation in long-term trend. Make no mistake about this key level. If it is breached on a closing basis, then a continued decline is the most likely broader outcome. However, this appears to be a remote possibility. An annual closing back above 7997 will confirm a breakout to the upside is unfolding into the years ahead. Nevertheless, we have penetrated last year’s low of 4606. A year end closing below 4606 will warn of a further decline ahead ideally into 2017.

In A$, the key monthly closing to watch lies at 4190. This is actually equivalent to the US$ number 3070. In terms of A$, wheat has also made a new low so far in 2016 reaching 5111 during August. We need a monthly closing back above 5733 to signal wheat will rise in A$ terms. The only thing to unleash that result requires the dollar to rise sharply.

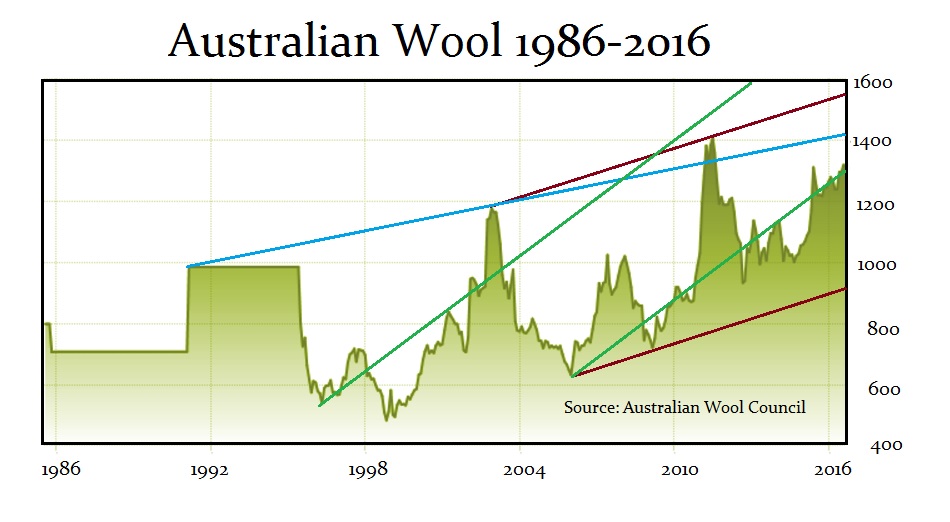

The Australian Wool market is poised to make new highs in nominal terms, but it is still nowhere near the 1951 high in real terms. The Australian wool industry peaked in 1950-51 when the average greasy wool price reached 144.2 pence per pound, (about $37 per kilogram). Today’s prices in the area of $3.20 per kilogram illustrate the stark difference. That major high in terms of wool was created by a two-prong influence. First, the British pound was devalued in 1949 from $4.86 to $2.80. The British demand for Australian wool had consumed about 50% of the annual production. The prices reached in 1950-1951 surged initially, as always, to reflect the devaluation of a currency. This was 9x the 1945-46 United Kingdom contract price, and almost 14x the average for the 10 seasons ending in 1938-39. Nonetheless, the rally in wool was also furthered by the short-lived surge in American demand created by the Korean War.

It is very clear that Australian Wool has been greatly influenced by the cycle in gold and thus mining. The low in wool coincided cyclically with gold in forming a 1999 low. The peak is also 2011 as was the case in gold. We are pushing against resistance at this point and we need to close above 1300 to maintain a bullish posture at year-end. However, unlike gold, the decline was confined to the two-year reaction phase. Therefore, wool is in a better position than gold. Breaking through the 2011 high should see the price test the high 1500s to 1600.

When we look at Wool expressed in US dollars, we can see the significant difference this makes. Overall, we do see 2017 as a potential turning point also for the wool market. Take the lead from wheat in A$ terms for now.

https://www.armstrongeconomics.com/markets-by-sector/agriculture/a-wheat-wool-the-outlook/

» utube MM&C 4/16/24 IQD Update - Iraq Dinar - America - Activate - Massive Economic Deals -

» utube MM&c 4/19/24 Iraqi Dinar - Private Sector - Economic Stability - Financial Reform - Al Sudan

» Iraq officially signs the “Singapore” agreement to resolve trade disputes

» Parliament Finance advises raising exchange rates again... What about oil revenues?

» Al-Sudani: Iraq is in the process of recovery and has taken its leading position that attracts work

» Al-Araji: Iraq is prepared to deal with all circumstances and seeks partnership with the United Stat

» Sudanese from Michigan: The government represents all components and is keen to take care of the aff

» Democratic Party: The "new generation" is the most corrupt and has dozens of cases in court

» What is the benefit of Iraq establishing a petrochemical plant in Egypt?!.. An oil expert explains

» A judicial delegation participates in the Permanent International Forum for Commercial Courts in Qat

» Al-Sudani: The government follows a balanced policy that makes Iraq a station for security

» Deduction of 160 million dinars from the salaries of MPs absent from Parliament sessions

» Central Bank: Washington praised Iraq's measures to resolve 80% of the financial transfer file

» Voices of Resilience: Al-Sudani’s frankness embarrasses the White House

» Al-Alaq confirms the formation of a committee between Baghdad and Washington regarding sanctions on

» Former MP: The Democrat will not hand over power after the regional elections

» Document/allocation of 20% of the lands of Al-Jawahiri Complex to employees of the Ministry of Defen

» Al-Hakim: Al-Sudani’s visit to Washington was a protocol and missed the two most important files

» Parliamentary Security: The National Security Service law will be voted on by Parliament soon

» Reconstruction and Housing: Zarbatieh residential project completed by 82%

» Al-Sudani reveals an intention to establish Al-Faw refinery with a capacity of 300 thousand barrels

» Government readiness to move the Doura refinery to an alternative location.. What are the conditions

» Al-Sudani’s visit to Washington.. Implications and results

» Association of Iraqi Private Banks: The suspension of some electronic payment services yesterday was

» Parliamentary memorandum.. Two solutions were before the Federal Court instead of removing the compo

» Blue fuel... Iraqi steps towards inexhaustible wealth for a century

» For fear of being "upset"... MPs "evade" signing to host Al-Sudani in Parliament

» Al-Sudani’s statement to convert 40% of Iraq’s exports into derivatives.. What does it have to do wi

» An Iraqi-American partnership to benefit from oil field gas

» The Minister of Commerce announces the distribution of the first payments of farmers’ dues for the 2

» Sudanese to members of the Iraqi community in the American city of Houston: Iraq has regained its he

» Romanski announces loans worth $50 million to support the Iraqi private sector

» Prime Minister: We plan to invest production capacities for export

» “Something happened” in Iran and no one is talking about Iraq and Syria. This is what we have so far

» Al-Sudani asks the American Baker Institute for assistance in preparing studies related to the oil m

» The Interior Ministry denies the occurrence of explosions inside Iraqi territory and diagnoses “the

» Tensions between Najaf and Baghdad over the airport... the rule of law over “military force” and the

» Al-Sudani from Washington: We agreed with Abu Dhabi on joint management of Al-Faw Port

» "Al-Party" talks about the region's elections and reveals the reason for refusing to pay salaries di

» Russia's oil is taking more of the Middle East's shares in the Indian market.. How much has Iraq los

» Early next month.. Traffic confirms that the electronic payment system is working only

» The Service Council accuses state departments of refraining from disbursing bonuses because of the m

» Electricity: The Baghdad street lighting campaign will be completed before the middle of this year

» Oil poses two conditions for moving the Doura refinery to an alternative location

» The Foreign Minister reveals the truth about his resignation and the reason for his departure to Erb

» Progress: Al-Halbousi’s acquittal has become conclusive, and his return to the presidency of Parliam

» Disagreements strike Al-Maliki's coalition over choosing the governor of Diyala

» The Union accuses Türkiye of exploiting the political situation for a ground incursion into Iraq

» The Democratic Party: Barzani is eagerly awaiting the results of Al-Sudani’s visit to Washington

» Frame: Al-Halbousi in the news and his return has become a pipe dream

» A parliamentary request to capitalize on Erdogan’s visit to Baghdad to end the water crisis

» Al-Sudani urges the US corporation Honeywell to help finish the Basra refinery

» Al-Sudani Meets with Representatives of Western Media Outlets in Washington

» Chairman of the Investment Authority signs the United Nations Convention on International Mediation

» PM: We will sign a contract to establish the Al-Faw refinery with a Chinese company

» PM arrives in Houston as part of his visit to USA

» Militia Man & Crew 4/18/24 Bush signed it and all presidents implemented it. Iraq’s funds have been

» Iraq is close to launching the electronic signature

» The Basra government discusses with an international oil company the implementation of social benefi

» The Prime Minister confirms to an American company: Gas projects in Iraq are a priority for the gove

» The Minister of Planning discusses with the World Bank mechanisms for scheduling external loans

» Oil sets the twenty-seventh of this month as the date for opening contracts for the fifth complement

» “Electronic begging”...professionalism and fabrication of stories” generates millions of dinars dail

» Al-Sudani calls on the American company Hanwell to contribute to the completion of the Basra refiner

» An American company expresses its willingness to establish LED lighting production lines in Iraq

» Including Iraq.. Iran announces the possibility of exporting 300 megawatts of “renewable electricity

» Political forces present two options to find an alternative to Al-Halbousi

» Parliament is awaiting the arrival of the budget schedules and the government is studying higher spe

» The International Monetary Fund adjusts its expectations for the development of the world’s economie

» A representative talks about the difficulty of finalizing the file of “electing the Speaker of Parli

» Work on preparing a law for diplomatic passports

» A female representative accuses the Ministry of Immigration of corruption

» Minister: Solving the Kurdistan salaries problem is the beginning of addressing other disputes betwe

» About 270 million dollars were sold by the Central Bank of Iraq in the currency auction

» The volume of trade exchange between Jordan and Iraq will exceed 800 million dinars in 2023

» Iraq signs memorandums of understanding with American companies in the fields of electricity, oil an

» The American company that manufactures the F16 expresses its readiness to implement the terms of con

» The volume of expected Qatari investments for the Iraq Fund for Development exceeds $3.5 billion

» Decrease in dollar prices in Baghdad and Erbil

» The President of the Region brings together the Kurdish parties to resolve the election file

» Al-Sudani receives in Washington the Chairman of JPMorgan

» Transport is starting to transform its ports into smart ones

» Sudanese reveals the volume of exchange with America

» "Al-Eqtisad News" publishes the memorandums of understanding signed between the Iraqi delegation and

» Al-Sudani urges an American company to contribute to establishing a chemical materials factory

» Iraq stresses the importance of Lockheed Martin's commitment to opening military aircraft maintenanc

» Iraq is on the verge of a “water disaster” by 2035

» Great satisfaction and optimism with the results of Sudanese’s visit to Washington

» Transport is beginning to adopt a plan to transform its ports into smart ones

» Completed 8,000 loan transactions at the Housing Bank

» Prime Minister: We plan to invest production capacities for export

» Transformation and partnership...a new horizon in Iraqi-American relations

» What is new in the economic dimension of the Washington visit?

» Two letters to the future

» National interests first

» Iraqi-American rapprochement...a national necessity

» Al-Sudani’s visit to Washington and the course of Iraqi-American relations

» Sudanese carries security, economic and development files to Washington