Yuan Enters SDR - Why its Reserve Currency Status Matters to Traders?

Friday, Sep 30, 2016 12:18 pm -07:00

by Renee Mu, Currency Analyst

Talking Points:

- The Yuan’s reserve currency status will likely further increase its trading volume

- The trading band and open market hours for onshore Yuan rates could be extended as well

- China’s economic growth and risks in financial markets are main drivers for Yuan rates

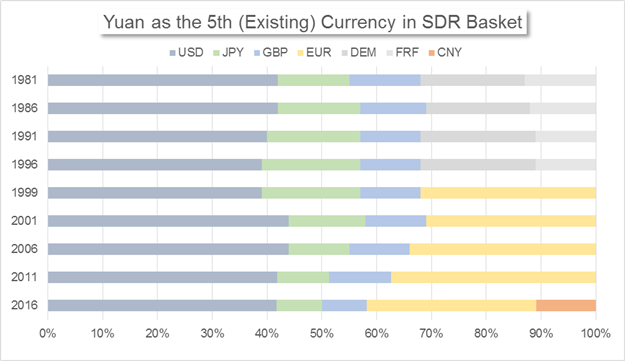

As of October 1st, the Chinese Yuan is officially included in the Special Drawing Right (SDR) basket, as the fifth primary reserve currency, with a weighting of 10.92%. The International Monetary Fund (IMF) announced the approval on November 30th, 2015, marking a milestone for the Chinese currency.

Central banks have already started to increase Yuan holdings as foreign reserves - on June 22nd, 2016, Singapore’s Monetary Authority announced it would include Yuan-denominated assets as part of its official foreign reserves. However, for traders and investors, the Yuan’s official reserve status could bring benefits in a different way.

Data downloaded from the IMF; chart prepared by Renee Mu.

Trading Volume

One of the most important advantages brought by the Yuan’s inclusion into the SDR basket is that the currency is legitimized and recognized as a safe and stable store of wealth by the financial world. Subsequently, trading volume in the Yuan is likely to increase as well, as access to the economy and popularity of its assets rise.

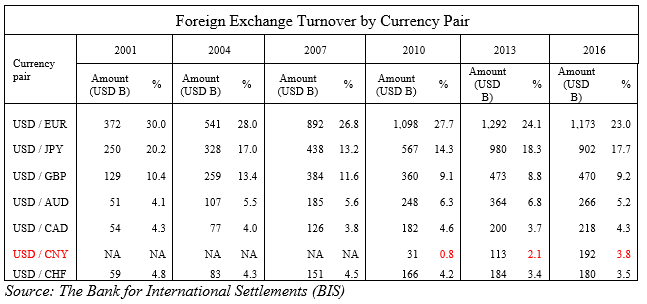

Let’s take a look at the evolution of the Yuan’s use. According to the Bank for International Settlements (BIS), information for USD/CNY trades before 2010 is not available. The BIS states that USD/CNY turnover for the period prior to 2013 may be underestimated due to incomplete reporting of offshore trading in previous surveys.

The lack of data and accuracy before 2013 may be caused by one of two reasons: A) the trading volume of the USD/CNY before 2010 may be so low that there is no need to account for it. B) There might be a descent amount of trading in the USD/CNY, but without enough recognition of the pair, it was not measured.

Now with the approval of SDR inclusion, the Chinese Yuan has become more recognized by the global banking community. In 2016, the USD/CNY has taken up 3.8% of the total trades measured by the BIS, rising from 2.1% in 2013; the weighting has exceeded that of the USD/CHF which is 3.5% in 2016.

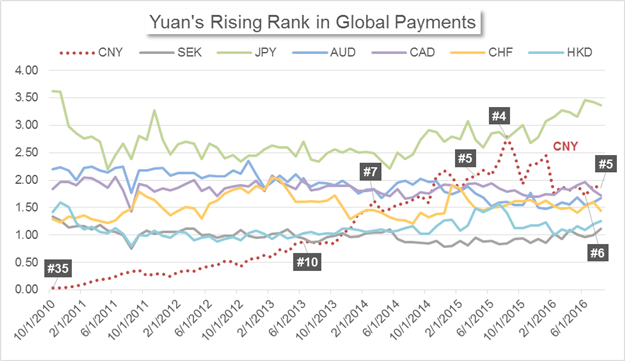

The Yuan’s role in global payments and settlements has been rising as well. According to the Society for Worldwide Interbank Financial Telecommunication (SWIFT), the Yuan’s ranking for international payments has been increasing quickly: the Chinese currency has overtaken 6 currencies over the past three years. The most recent report from the SWIFT shows that the Chinese Yuan accounted for 1.86% of global payments in August; ranking it fifth after the U.S. Dollar, the Euro, the British Pound and the Japanese Yen - the other four currencies included in the SDR basket.

Data downloaded from Bloomberg; chart prepared by Renee Mu.

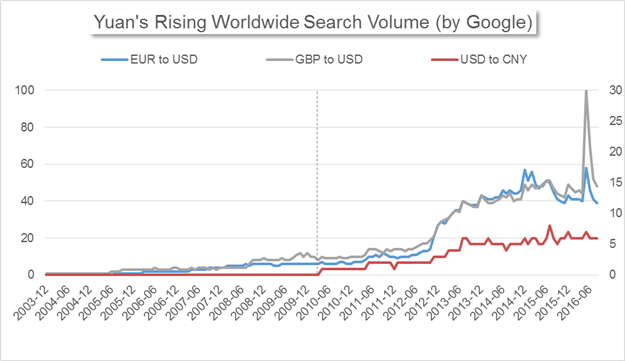

A report from Google Trends adds more evidence to the increasing popularity in the Dollar/Yuan exchange rate. The leading search engine evaluates how often a particular term is searched by worldwide users and gives it a rating from 0 (lowest) to 100 (highest). In the following chart, the search volume for ‘GBP to USD’ (same for ‘USD to GBP’) in May 2016 is set as the highest level and given a score of 100; this is likely driven by heated discussions before the Brexit referendum. Compare to the highest search volume, the amount of global users looking into ‘USD to CNY’ (same for ‘CNY’ to ‘USD’) was extremely low before 2010, and therefore was given a score of 0.

From the middle of 2010, the search volume for ‘USD to CNY’ started to pick up and has been gradually increasing over the following four years. Although the popularity in the USD/CNY is still relatively low compared to the established ‘major pairs’ - such as EUR/USD or GBP/USD - it has gained quickly.

Data downloaded from Google; chart prepared by Renee Mu.

For traders, the increase in trading volume for Yuan pairs is good news. To learn about the various names of the Chinese currency and differences between onshore and offshore Yuan rates, read All About The Yuan.

Trading Band and Hours

The Chinese currency is not yet ‘free floating’. Onshore Yuan pairs are allowed to move within a certain range, determined by China’s Central Bank. The current trading band is 2% above or below Yuan’s reference rate, which is set by the Central Bank on a daily basis. For traders, the trend of the trading band may be more important than the level itself.

We can see from the chat below, it took 13 years for Yuan’s trading band to increase by +0.2% to 0.5% in 2007. However, it more recently only took 2 years for the band to increase by +1.0% to 2.0% in 2014. Both the frequency and degree of changes in the trading band have increased significantly. We may see additional expansion in the trading band driven by the momentum of the Yuan’s rise.

Data downloaded from The People’s Bank of China; chart prepared by Renee Mu.

A larger trading band means a higher level of maximum volatility. Traders will want to keep in mind that greater volatility may bring larger risks of loss as well as higher potential returns.

In addition to the broadening trading band, trading hours for Yuan rates have also been extended. Beginning on January 4th, 2016, China’s Central Bank has expandedthe onshore Yuan’s trading by additional seven hours, in the effort of facilitating traders in European and American time zones.

Be Aware of Major Themes in China When Trade the Yuan

China’s economic growth and risks to its financial markets are primary drivers for the Yuan rates from a fundamental point of view. In terms of technical analysis, read our Sr. Technical Strategist Jamie Saettele’s weekly forecast for the USD/CNH pair.

The Economic Slowdown

The health of a country’s economy lays the foundation for its currency and affects the currency’s long-term trend. For the Chinese Yuan, as it was linked to the U.S. Dollar to varying degrees before August 11th, 2015, Yuan rates may not fully reflect the real condition of the Chinese economy.

After being de-pegged, the Yuan exchange rate garnered greater flexibility and thus may better reflect the real economy. China’s growth has dropped to 6.7% in 2016 from 12.2% in the first quarter of 2010, a post-financial-crisis high.

Data downloaded from Bloomberg; chart prepared by Renee Mu.

In terms of the outlook for the economy, China’s policy leaders said that ‘the trend in the current and following periods is L-shaped, rather than U-Shaped’. In specific, the economy will likely reach the bottom within one or two years and then stay there for quite a significant amount of time before pickingback up again. This doesn’t mean that Yuan rates may not rise in the short or medium-term, driven by various internal and external factors; yet, in a longer time frame, the slowing economy may provide limited support to the currency.

The Risk of Housing Price Bubbles

China’s economic policy is one of the key drivers to Yuan rates. Currently, the country employs moderate monetary policy and proactive fiscal policy; this will likely continue to be the case amid the increasing risk of price bubbles and a lack of investment opportunities in the private sector.

The New Yuan Loans prints for July and August show that a majority of new credit issued has flown into the real estate sector. At the same time, a large amount of companies and individuals hold excessive cash on their hand as they are short onother investment opportunities. This indicates that home purchasers and real estate developers are the main group that want to borrow and spend in China. Within such a context, additional easing measures are less likely to generate diversified investment or business expansion, but more likely to fuel bubbles in the housing sector.

With low odds of the PBoC cutting rates in the near term, the Yuan may bear less devaluation pressure from home. The Chinese government is aware of the risk of price bubbles in the real estate sector and the shortage of viable investments; regulators have been working on these issues through efforts like promotingPublic-Private-Partnership projects. As individuals and companies become more willing to invest in a broader scope, the PBoC may then shift the tone on monetary policy. China’s daily news will cover these developments and help DailyFX readers to catch early signals that may hint at changes in monetary policy.

Other Ongoing Themes in China

There are other major ongoing themes worth keeping an eye on:

China is implementing major productions cuts in the manufacturing industry -one of the five goals for 2016- and Chinese manufacturing firms are facing challenges to meet the target by the end of the year.

Defaults in Chinese state-owned-enterprises (SOEs) have been increasing significantly in 2016. In May, energy firms started to miss payments on their debts. By August, the default risk has spread around Northeast China. One of the major solutions to help SOEs reduce debt is to swap debt into equities: after long discussions on the eligibility of participating firms, regulators finally approved the first deal for a SOE in September.

https://www.dailyfx.com/forex/fundamental/article/special_report/2016/09/30/Yuan-Enters-SDR-Why-its-Reserve-Currency-Status-Matters-to-Traders.html?utm_source=AWeber&utm_medium=Mu&utm_campaign=em

Friday, Sep 30, 2016 12:18 pm -07:00

by Renee Mu, Currency Analyst

Talking Points:

- The Yuan’s reserve currency status will likely further increase its trading volume

- The trading band and open market hours for onshore Yuan rates could be extended as well

- China’s economic growth and risks in financial markets are main drivers for Yuan rates

As of October 1st, the Chinese Yuan is officially included in the Special Drawing Right (SDR) basket, as the fifth primary reserve currency, with a weighting of 10.92%. The International Monetary Fund (IMF) announced the approval on November 30th, 2015, marking a milestone for the Chinese currency.

Central banks have already started to increase Yuan holdings as foreign reserves - on June 22nd, 2016, Singapore’s Monetary Authority announced it would include Yuan-denominated assets as part of its official foreign reserves. However, for traders and investors, the Yuan’s official reserve status could bring benefits in a different way.

Data downloaded from the IMF; chart prepared by Renee Mu.

Trading Volume

One of the most important advantages brought by the Yuan’s inclusion into the SDR basket is that the currency is legitimized and recognized as a safe and stable store of wealth by the financial world. Subsequently, trading volume in the Yuan is likely to increase as well, as access to the economy and popularity of its assets rise.

Let’s take a look at the evolution of the Yuan’s use. According to the Bank for International Settlements (BIS), information for USD/CNY trades before 2010 is not available. The BIS states that USD/CNY turnover for the period prior to 2013 may be underestimated due to incomplete reporting of offshore trading in previous surveys.

The lack of data and accuracy before 2013 may be caused by one of two reasons: A) the trading volume of the USD/CNY before 2010 may be so low that there is no need to account for it. B) There might be a descent amount of trading in the USD/CNY, but without enough recognition of the pair, it was not measured.

Now with the approval of SDR inclusion, the Chinese Yuan has become more recognized by the global banking community. In 2016, the USD/CNY has taken up 3.8% of the total trades measured by the BIS, rising from 2.1% in 2013; the weighting has exceeded that of the USD/CHF which is 3.5% in 2016.

The Yuan’s role in global payments and settlements has been rising as well. According to the Society for Worldwide Interbank Financial Telecommunication (SWIFT), the Yuan’s ranking for international payments has been increasing quickly: the Chinese currency has overtaken 6 currencies over the past three years. The most recent report from the SWIFT shows that the Chinese Yuan accounted for 1.86% of global payments in August; ranking it fifth after the U.S. Dollar, the Euro, the British Pound and the Japanese Yen - the other four currencies included in the SDR basket.

Data downloaded from Bloomberg; chart prepared by Renee Mu.

A report from Google Trends adds more evidence to the increasing popularity in the Dollar/Yuan exchange rate. The leading search engine evaluates how often a particular term is searched by worldwide users and gives it a rating from 0 (lowest) to 100 (highest). In the following chart, the search volume for ‘GBP to USD’ (same for ‘USD to GBP’) in May 2016 is set as the highest level and given a score of 100; this is likely driven by heated discussions before the Brexit referendum. Compare to the highest search volume, the amount of global users looking into ‘USD to CNY’ (same for ‘CNY’ to ‘USD’) was extremely low before 2010, and therefore was given a score of 0.

From the middle of 2010, the search volume for ‘USD to CNY’ started to pick up and has been gradually increasing over the following four years. Although the popularity in the USD/CNY is still relatively low compared to the established ‘major pairs’ - such as EUR/USD or GBP/USD - it has gained quickly.

Data downloaded from Google; chart prepared by Renee Mu.

For traders, the increase in trading volume for Yuan pairs is good news. To learn about the various names of the Chinese currency and differences between onshore and offshore Yuan rates, read All About The Yuan.

Trading Band and Hours

The Chinese currency is not yet ‘free floating’. Onshore Yuan pairs are allowed to move within a certain range, determined by China’s Central Bank. The current trading band is 2% above or below Yuan’s reference rate, which is set by the Central Bank on a daily basis. For traders, the trend of the trading band may be more important than the level itself.

We can see from the chat below, it took 13 years for Yuan’s trading band to increase by +0.2% to 0.5% in 2007. However, it more recently only took 2 years for the band to increase by +1.0% to 2.0% in 2014. Both the frequency and degree of changes in the trading band have increased significantly. We may see additional expansion in the trading band driven by the momentum of the Yuan’s rise.

Data downloaded from The People’s Bank of China; chart prepared by Renee Mu.

A larger trading band means a higher level of maximum volatility. Traders will want to keep in mind that greater volatility may bring larger risks of loss as well as higher potential returns.

In addition to the broadening trading band, trading hours for Yuan rates have also been extended. Beginning on January 4th, 2016, China’s Central Bank has expandedthe onshore Yuan’s trading by additional seven hours, in the effort of facilitating traders in European and American time zones.

Be Aware of Major Themes in China When Trade the Yuan

China’s economic growth and risks to its financial markets are primary drivers for the Yuan rates from a fundamental point of view. In terms of technical analysis, read our Sr. Technical Strategist Jamie Saettele’s weekly forecast for the USD/CNH pair.

The Economic Slowdown

The health of a country’s economy lays the foundation for its currency and affects the currency’s long-term trend. For the Chinese Yuan, as it was linked to the U.S. Dollar to varying degrees before August 11th, 2015, Yuan rates may not fully reflect the real condition of the Chinese economy.

After being de-pegged, the Yuan exchange rate garnered greater flexibility and thus may better reflect the real economy. China’s growth has dropped to 6.7% in 2016 from 12.2% in the first quarter of 2010, a post-financial-crisis high.

Data downloaded from Bloomberg; chart prepared by Renee Mu.

In terms of the outlook for the economy, China’s policy leaders said that ‘the trend in the current and following periods is L-shaped, rather than U-Shaped’. In specific, the economy will likely reach the bottom within one or two years and then stay there for quite a significant amount of time before pickingback up again. This doesn’t mean that Yuan rates may not rise in the short or medium-term, driven by various internal and external factors; yet, in a longer time frame, the slowing economy may provide limited support to the currency.

The Risk of Housing Price Bubbles

China’s economic policy is one of the key drivers to Yuan rates. Currently, the country employs moderate monetary policy and proactive fiscal policy; this will likely continue to be the case amid the increasing risk of price bubbles and a lack of investment opportunities in the private sector.

The New Yuan Loans prints for July and August show that a majority of new credit issued has flown into the real estate sector. At the same time, a large amount of companies and individuals hold excessive cash on their hand as they are short onother investment opportunities. This indicates that home purchasers and real estate developers are the main group that want to borrow and spend in China. Within such a context, additional easing measures are less likely to generate diversified investment or business expansion, but more likely to fuel bubbles in the housing sector.

With low odds of the PBoC cutting rates in the near term, the Yuan may bear less devaluation pressure from home. The Chinese government is aware of the risk of price bubbles in the real estate sector and the shortage of viable investments; regulators have been working on these issues through efforts like promotingPublic-Private-Partnership projects. As individuals and companies become more willing to invest in a broader scope, the PBoC may then shift the tone on monetary policy. China’s daily news will cover these developments and help DailyFX readers to catch early signals that may hint at changes in monetary policy.

Other Ongoing Themes in China

There are other major ongoing themes worth keeping an eye on:

China is implementing major productions cuts in the manufacturing industry -one of the five goals for 2016- and Chinese manufacturing firms are facing challenges to meet the target by the end of the year.

Defaults in Chinese state-owned-enterprises (SOEs) have been increasing significantly in 2016. In May, energy firms started to miss payments on their debts. By August, the default risk has spread around Northeast China. One of the major solutions to help SOEs reduce debt is to swap debt into equities: after long discussions on the eligibility of participating firms, regulators finally approved the first deal for a SOE in September.

https://www.dailyfx.com/forex/fundamental/article/special_report/2016/09/30/Yuan-Enters-SDR-Why-its-Reserve-Currency-Status-Matters-to-Traders.html?utm_source=AWeber&utm_medium=Mu&utm_campaign=em

» utube 11/13/24 MM&C MM&C News-Private Sector- Electronic Payments-Reconstruction-Development-Digit

» utube MM&C 11/15/24 Update-Budget-Non Oil Resources-CBI-USFED-Cross Border Transfers-Oil

» Al-Sudani is besieged by lawsuits over the “wiretapping network”... and Al-Maliki heard “inappropria

» Tens of thousands of foreigners work illegally in Basra... and the departments will bear the respons

» 4 reasons for the Sudanese government’s silence in the face of the factions’ attacks.. Will Baghdad

» PM's advisor: Government able to increase spending without inflation or fiscal deficit

» Prime Minister stresses the need to complete 2024 projects before the end

» Minister of Labor sets date for launching second batch of social protection beneficiaries in the pol

» Al-Sudani approves 35 new service projects, stresses the need to complete 2024 projects

» Minister of Labor: The population census will provide accurate calculations of poor families covered

» Electricity announces its readiness for the winter peak

» Economist: Parallel market remains pivotal to financing Iraq’s trade with Iran, Syria

» Trump: Iraq: A subsidiary or the focus of major deals?

» Counselor Mazhar Saleh: The government is able to increase spending without causing inflation or a f

» Al-Sudani's advisor to "Al-Maalouma": We do not need to bring in foreign workers

» Parliamentary Rejection.. Parliamentarian Talks About Jordanian Agreement That Harms Iraq’s Economy

» Al-Sudani chairs the periodic meeting of the service and engineering effort team

» Al-Sahaf: Washington continues to support terrorist organizations in Iraq

» Al-Maliki Coalition: America is trying to make Iraq hostile to its neighbors by violating its airspa

» Close source: Al-Sudani failed to convince Al-Hakim and Al-Amiri to carry out the ministerial reshuf

» Al-Sayhoud on Postponing Parliament Sessions: Bad Start for Al-Mashhadani

» Peshmerga Minister: The survival of the Kurdistan Region depends on the presence of a strong Peshmer

» Al-Maliki Coalition: US pressures prevent Israel from striking Iraq

» Nechirvan Barzani calls for keeping Peshmerga out of partisan conflicts, urges formation of 'strong

» US Institute: Trump administration may prevent Iraq from importing Iranian gas as part of pressure o

» The meter will visit families again.. Planning details the steps for conducting the population censu

» Government clarification: Is Iraq able to increase spending?

» Iraq advances over China.. Iran's trade exchange witnesses growth during October

» Al-Sudani approves 35 new service projects and begins implementing them within 10 days

» Al-Sudani and Al-Hakim discuss developments in the political scene and the results of the visit to K

» Minister of Labor: Government measures contributed to reducing the poverty rate from 22% to 16.5%

» Al-Maliki calls for strengthening national dialogue and unity to overcome the current stage

» Al-Sudani stresses the importance of accuracy and specifications in service and engineering projects

» Baghdad Governor: 169 projects are listed for referral and contracting

» Industry confirms success by signing 4 investment contracts for strategic industries

» Parliament confirms its support for conducting the general population census and decides to resume s

» Parliament gains a "holiday and a half"... Half of the "extended" legislative term passes without se

» Find out the exchange rates of the dollar against the dinar in the Iraqi stock exchanges

» Al-Maliki describes tribes as a "pillar" for confronting challenges in Iraq

» The plan in the "distribution method".. A representative describes the "investment achievement" as n

» Iraq is ahead of China in trade exchange with Iran.. These are the numbers

» MM&C 11/14/24 Central Bank Governor Urges Türkiye to Open Accounts for Iraqi Banks

» MM&C 11/14/24 Trump and the Iraqi Banks Puzzle

» New decline in gold in Iraq.. and globally records the worst week in 3 years

» Monitoring body approves 2023 imports annual report

» Development Road: Faw Port Ignites Regional Corridor Race

» First in Iraq... Diyala sets a plan for "rural reconstruction"

» Al-Saadi: Influential parties are working to erase the theft of the century file

» MP: Baghdad supports the "Diyala Artery" project with 40 billion dinars

» Source: General amnesty law will pave the way for the return of terrorist groups

» The Prime Minister stresses the need to expedite the completion of the requirements for restructurin

» Minister of Resources: The project to develop the left side of the Tigris River has reached its fina

» Foreign Minister: We are proceeding with implementing the associated gas exploitation program

» Swiss Ambassador Expresses His Country's Desire to Invest in Iraq

» "We left the camel and its load" .. Moroccan farmers await "imminent compensation" from Iraq

» OPEC sues Iraqi minister over oil violations.. What is Kurdistan's involvement?

» Iraq warns of 'dire consequences' of imposing barriers to plastic products

» Iranian newspaper: Iraq's development path is a step towards regional economic integration

» Al-Mandlawi discusses with the Russian ambassador developing relations in the fields of economy, inv

» Oil Minister discusses with Dutch Ambassador strengthening bilateral relations

» The Minister of Oil discusses with the companies "+dss" and "Xergy", joint cooperation to develop th

» Rafidain Bank announces a plan to include other branches in the implementation of the comprehensive

» With the presence of the opposition... Baghdad supports the partnership government in Kurdistan

» Parliamentary move to raise retirement age in state institutions to 63 years

» Through leaks.. Warnings against creating political crises as parliamentary elections approach

» Iraqi oil returns to decline in global markets

» Parliamentary Committee: Iraq uses its international relations to avert the dangers of war from its

» The value of non-oil imports for Sulaymaniyah and Halabja governorates during a week

» Rafidain: Continuous expansion in implementing the comprehensive banking system

» Planning: The population census includes residents of Iraq according to a special mechanism

» Transparency website reveals non-oil imports to Sulaymaniyah and Halabja during a week

» Al-Sudani directs the adoption of specialized international companies to prepare a unified structure

» MP warns of a move that will worsen the housing crisis and calls on the government

» Disagreements strike the Kurdish house... hindering the formation of the regional parliament and gov

» Hundreds of Moroccan farmers are waiting for “imminent compensation” from Iraq.. What’s the story?

» Iraq 10-Year Review: Spending, Imports, Unemployment in 2024 at ‘Highest Level’ in a Decade

» Call to all smokers in Iraq: Prepare for the law

» utube 11/11/24 MM&C News Reporting-IRAQ-USA-Financial Inclusion up 48%-Money Inside & Out of Iraq

» Al-Mandlawi to the UN envoy: The supreme authority diagnosed the problems and provided solutions for

» Saleh: Government strategy to boost gold reserves as part of asset diversification

» Prime Minister's advisor rules out oil price collapse: Trump's policy will not sacrifice petrodollar

» Tripartite alliance between Iraq, Egypt and Jordan to boost maritime trade

» Parliamentary Committee reveals date of entry into force of Personal Status Law

» Al-Fatah warns against US blackmail and Trump's intentions for the next stage

» A leader in the law: If the Americans do not leave on their own two feet, we will expel them in fune

» MP: Next Sunday's session will witness the passing of "important laws"

» There is a financial aspect.. Al-Zaidi rules out voting on the real estate law

» "Promising" economic opportunities in central Iraq open doors to investment, trade and unemployment

» Minister of Transport: Arab interest in the development road project

» Bitcoin Fails to Maintain Its Meteoric Rise

» Amending the retirement age on the parliament's table.. This is the latest that has been reached

» Launching the Health Unit Initiative in Iraqi Schools

» Will Iraq be the savior of the countries of the region if oil prices fall?

» Regarding electrical energy.. Government moves to meet the needs of next summer

» {Retirement age} sparks debate in parliament

» Minister of Transport to {Sabah}: Arab interest in the development road project

» Planning: Two important pre-census activities start today and tomorrow

» Next week.. contracting with 2500 applicants on a {contract} basis