The Markets Opening August 25, 2015

Posted on August 25, 2015 by Martin Armstrong

The world share markets remain volatile yet should begin to stabilize now showing tentative signs that the panic of Monday is starting to subside. The reported epicenter of Shanghai for the rout, however, has suffered another big sell-off. The mayhem in China’s equity markets showed no signs of abating on Tuesday, as the Shanghai Composite index accelerating its downfall in the afternoon trading session to settle below the key 3,000 psychological mark.

In Tokyo, Japan’s Nikkei 225 index was the second-biggest loser in the region, closing down 4% after turning negative late in the day. Going into the lunch break, the Tokyo market staged a comeback along with most of the other Asian stock indices. To some extent, this was supported by the fact that the Dow Jones Industrial Average futures opened up more than 100 points Monday evening. As noted before, the sell-off in the US market into the close illustrated the crack in confidence and it was a better position to leave the market appearing weak rather the strong for the close. A strong close would have encouraged people to hold whereas a weak close shakes the weak players out of the tree.

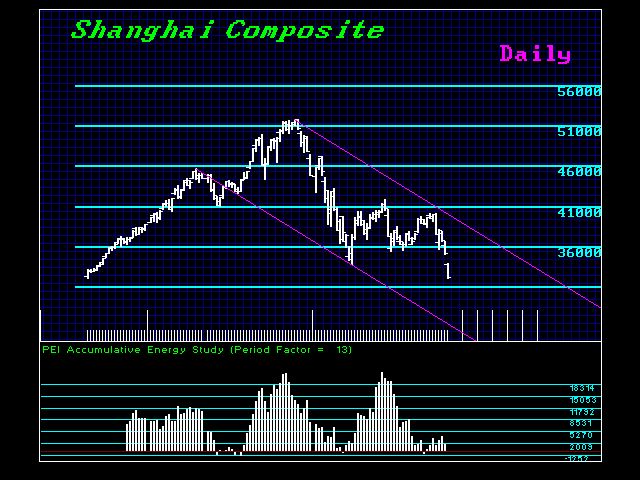

The Shanghai charts are a completely different technical perspective from the rest of the world. Here, the market had to move back down to test the bottom of the channel. There was just no technical support to cling to in mid-air. Consequently, there should be some decoupling since the sell-off was not really caused by China, but total global confusion. This is raising hopes as the day unfolds around the world that Monday’s low in the USA may indeed hold.

Name …………………………………….Price Change %Change

Nikkei 225 Index …………………… 17806.70 -733.98 -3.96%

Hang Seng Index ………………….. 21037.48 -214.09 -1.01%

S&P/ASX 200…………………………. 5137.30 136.02 2.72%

Shanghai Composite Index………. 2960.40 -249.51 -7.77%

KOSPI Index………………………….. 1846.63 16.82 0.92%

In the previous session, the Shanghai bourse nosedived nearly 9% to make its biggest one-day percentage loss since 2007, which many are now calling “Black Monday”.

Analysts attributed the market crash to the erosion of confidence among investors coming in from overseas traders. Indeed, China’s devaluation rattled foreign investors, for that was effectively a tax on such an investment. Chinese regulators indeed have enormous resources and tools to normalize the market according to investor expectations, as was the case in Japan. People tend to think in conspiracy terms that there are actually plunge protection teams in place by all governments. The rude awakening that such conspiracy theories are total BS shook investor’s confidence, disappointing them when the policy responses from China thus far were absent. There was a growing sense that the government responses have been unorthodox, ineffective, and unhealthy for the long-term functioning of the Chinese capital markets. This is the classic blame game to try to explain events as always being under someone’s control when it is not.

There is no easy explanation to create confidence once again in the markets as we head into September. Hence, the meltdown in the Chinese mainland markets is likely to continue in a volatile and choppy pattern, which indicates that significant downside risks remain.

European shares are expected to open higher, with spread betters expecting more than 2 percent gains in Germany’s DAX and a rise of above 1% in Britain’s FTSE. China’s economy continues to slow and the U.S. Fed is still likely to raise rates before the end of the year. The Fed’s problem is that the low interest rates are creating the next crisis — bankruptcy in pension funds, especially public at the state and municipal levels. The Fed’s low rates have been kept there for far too long as an accommodation to Europe. The banking crisis has been long over in the USA and low rates have hurt so many areas that the Fed has lost all control of the economy where they have been boxed in by low rates, which have been exploited outside the USA with more than $9 trillion in dollar denominated debt created among emerging markets.

Even in China, players have been borrowing dollars in Hong Kong and taking the money home, helping to confuse analysts that China’s exports were not so bad. But with expectation of the Fed’s coming rate hike, many of those loans were in trouble and this too contributed to the Chinese “Black Monday” as Chinese investors sold to cover dollar loans that suddenly jump by the devaluation in addition to the expectation of rising interest rates. China’s devaluation helped to curb the rush of foreign investors into China, but it also helped to curb Chinese investors from borrowing dollars for speculation in China.

This entry was posted in China's Current Economy, The Global Market and tagged China's Black Monday, China's Devaluation, Fed Rate Hike, Pensions by Martin Armstrong. Bookmark the permalink.

http://www.armstrongeconomics.com/archives/36481

Posted on August 25, 2015 by Martin Armstrong

The world share markets remain volatile yet should begin to stabilize now showing tentative signs that the panic of Monday is starting to subside. The reported epicenter of Shanghai for the rout, however, has suffered another big sell-off. The mayhem in China’s equity markets showed no signs of abating on Tuesday, as the Shanghai Composite index accelerating its downfall in the afternoon trading session to settle below the key 3,000 psychological mark.

In Tokyo, Japan’s Nikkei 225 index was the second-biggest loser in the region, closing down 4% after turning negative late in the day. Going into the lunch break, the Tokyo market staged a comeback along with most of the other Asian stock indices. To some extent, this was supported by the fact that the Dow Jones Industrial Average futures opened up more than 100 points Monday evening. As noted before, the sell-off in the US market into the close illustrated the crack in confidence and it was a better position to leave the market appearing weak rather the strong for the close. A strong close would have encouraged people to hold whereas a weak close shakes the weak players out of the tree.

The Shanghai charts are a completely different technical perspective from the rest of the world. Here, the market had to move back down to test the bottom of the channel. There was just no technical support to cling to in mid-air. Consequently, there should be some decoupling since the sell-off was not really caused by China, but total global confusion. This is raising hopes as the day unfolds around the world that Monday’s low in the USA may indeed hold.

Name …………………………………….Price Change %Change

Nikkei 225 Index …………………… 17806.70 -733.98 -3.96%

Hang Seng Index ………………….. 21037.48 -214.09 -1.01%

S&P/ASX 200…………………………. 5137.30 136.02 2.72%

Shanghai Composite Index………. 2960.40 -249.51 -7.77%

KOSPI Index………………………….. 1846.63 16.82 0.92%

In the previous session, the Shanghai bourse nosedived nearly 9% to make its biggest one-day percentage loss since 2007, which many are now calling “Black Monday”.

Analysts attributed the market crash to the erosion of confidence among investors coming in from overseas traders. Indeed, China’s devaluation rattled foreign investors, for that was effectively a tax on such an investment. Chinese regulators indeed have enormous resources and tools to normalize the market according to investor expectations, as was the case in Japan. People tend to think in conspiracy terms that there are actually plunge protection teams in place by all governments. The rude awakening that such conspiracy theories are total BS shook investor’s confidence, disappointing them when the policy responses from China thus far were absent. There was a growing sense that the government responses have been unorthodox, ineffective, and unhealthy for the long-term functioning of the Chinese capital markets. This is the classic blame game to try to explain events as always being under someone’s control when it is not.

There is no easy explanation to create confidence once again in the markets as we head into September. Hence, the meltdown in the Chinese mainland markets is likely to continue in a volatile and choppy pattern, which indicates that significant downside risks remain.

European shares are expected to open higher, with spread betters expecting more than 2 percent gains in Germany’s DAX and a rise of above 1% in Britain’s FTSE. China’s economy continues to slow and the U.S. Fed is still likely to raise rates before the end of the year. The Fed’s problem is that the low interest rates are creating the next crisis — bankruptcy in pension funds, especially public at the state and municipal levels. The Fed’s low rates have been kept there for far too long as an accommodation to Europe. The banking crisis has been long over in the USA and low rates have hurt so many areas that the Fed has lost all control of the economy where they have been boxed in by low rates, which have been exploited outside the USA with more than $9 trillion in dollar denominated debt created among emerging markets.

Even in China, players have been borrowing dollars in Hong Kong and taking the money home, helping to confuse analysts that China’s exports were not so bad. But with expectation of the Fed’s coming rate hike, many of those loans were in trouble and this too contributed to the Chinese “Black Monday” as Chinese investors sold to cover dollar loans that suddenly jump by the devaluation in addition to the expectation of rising interest rates. China’s devaluation helped to curb the rush of foreign investors into China, but it also helped to curb Chinese investors from borrowing dollars for speculation in China.

This entry was posted in China's Current Economy, The Global Market and tagged China's Black Monday, China's Devaluation, Fed Rate Hike, Pensions by Martin Armstrong. Bookmark the permalink.

http://www.armstrongeconomics.com/archives/36481

» MM&C 4/25/24 National Bank of Iraq goes live with Temenos core banking and payments

» utube MM&C 4/26/24 Iraqi Dinar - US Treasury Exchange Rates- Focus - Banking Partnerships - Rate C

» A banking official indicates a "danger" to Iraq by depriving more than half of its banks of dollars

» With the participation of the Association of Private Banks, investment opportunities are on the tabl

» Within a month... an Iranian border crossing recorded a noticeable increase in exports of goods to I

» The Association of Private Banks appreciates the efforts of the government and the Central Bank to c

» Al-Maliki's coalition presents a third candidate for the position of governor of Diyala

» Arab gathering: The Kirkuk problem is getting complicated and the Sudanese must intervene

» Next week.. a Kurdish delegation will visit Baghdad to meet with the Minister of Finance

» Under the pretext of salaries... Al-Party refrains from handing over port revenues to Baghdad

» Association of Banks: For the first time, we are witnessing a clear targeting of depriving half of t

» Parliament does not know the reason for the delay in sending the 2024 budget schedules: Voting takes

» Applicants for the 2024 Hajj are demanding that the Central Bank secure the dollar for them through

» Governmental and private banks will showcase their services tomorrow during Financial Inclusion Week

» Iraq's oil exports rise despite OPEC+ cuts

» A study explodes a "surprise"... Iraq is among the countries that export oil to "Israel": How is the

» Al-Araji emphasizes working to strengthen national identity

» Al-Sudani visits Saudi Arabia to participate in the World Economic Forum in Riyadh

» Iraq is talking about producing one million additional liters of gasoline

» The Council of Ministers approves the implementation of the Baghdad Metro project

» Minister of Commerce: We formed a joint economic committee with Türkiye

» Resources: Government measures have contributed to improving the water situation in Iraq

» Parliamentary Finance: Baghdad will continue to send salaries to the region’s employees until settle

» A parliamentarian describes the corruption of Iraqi ports as “ghouls” and reveals the involvement of

» Obelisk Hour: Basra is the subject of political conflict and ambiguity over the fate of the funds al

» Turkmen leader: An agreement on the local government of Kirkuk is near

» Anbar calls for the operation of its factories despite financial obstacles

» Turki: The crisis of the Presidency of Parliament prompted the Sunnis to amend the Council’s interna

» The Agriculture Committee confirms the existence of Iraqi-Turkish-Iranian discussions on water

» Resources diagnose the challenges facing the water file in Iraq

» Parliament pledges to the Interior Ministry: We will transfer money to buy weapons from citizens

» Al-Issawi is the closest.. Parliament sets the date for deciding the choice of the new president

» Deputy: Iraq's investments have risen and need a comprehensive review of previous years

» Iraqis consume 7 billion eggs annually and import about $900 million

» The Iranian role complicates attempts at open cooperation between Iraq and Turkey. Turkey is trying

» Move in Iran to obtain $242 billion from Iraq in compensation for the eight-year war

» 12 decisions from the Council of Ministers regarding the Baghdad Metro and Najaf-Karbala train proje

» Sudanese Advisor: The path to development has begun... the Baka and the militias “we silence them wi

» Not from Kurdistan.. How did Iraq become a source of oil for “Israeli tanks”?

» Parliamentary Agriculture criticizes the Sudanese and Erdogan agreement: Türkiye will control water

» The Iraqi government issues new decisions

» The story of “reduced oil” to Jordan, from “compulsion” to mutual benefit.. Is there a loss?

» The Council of Ministers takes 12 decisions for the Baghdad Metro and the Najaf-Karbala train

» utube MM&C 4/23/24 Iraqi Dinar - IQD Update - Development Road Project - Saviour of Global Banking

» Kidney from pig transplanted into deathly ill New Jersey woman — and begins working almost immediat

» The most difficult option.. Warnings of the danger of floating the Iraqi dinar without achieving an

» Trade from the “Economic Committee” with Türkiye: It will overcome all obstacles facing the traders

» Washington's hope for stable relations with Baghdad clashes with Iraqi parties' rejection of the Ame

» Karim Badr: Development is America’s will to kill silk

» Oil: Opening of a new port for liquid gas for vehicles in Baghdad

» A media advisor warns of corruption in a draft law on the Parliament’s agenda

» Economist: There is serious work to lift US sanctions on Iraqi banks

» Will the agreements signed with the US Treasury reflect positively on the exchange rates?

» Iraq continues its quest to join the World Trade Organization

» Iraq completes the completion of the files for the initial offer of goods and services to join the W

» Economist: Travelers' dollars are leaking into the parallel market...and this is what the Central Ba

» President of the Federal Court: It is not permissible to force anyone to join any party, and the pol

» The Council of Ministers holds its session headed by Al-Sudani

» America weakens Baghdad...and increases Kurdistan's military capabilities

» The Iraqi government plans to build 10,000 schools throughout the country

» American threats close the Iraqi Stock Exchange at a loss

» Increase in external transfers at the Central Bank

» Al-Maliki calls on Britain to cancel restrictions on the entry of its companies into Iraq

» Planning and the European Union are discussing signing a number of agreements in the development, en

» Parliament talks about the mechanism for recovering smuggled funds and hints at the next stage

» Interior Ministry: The number of completed national cards reached 37 million cards

» Amnesty International: Violations of freedom and human rights continue in Iraq and the Kurdistan Reg

» Parliamentary Oil: The government is proceeding with the decision to raise the price of improved gas

» A parliamentary committee in Basra to investigate violations of the port company and the local gover

» Revealing the 10 most important American exports to Iraq

» A noticeable increase in the rate of Iraq's import of Chinese cooling devices

» Prime Minister: Working on projects without completing the infrastructure is a waste of money

» Iraq.. Extending the deadline for registration procedures on plots of land

» What is the main purpose of conducting the population census in Iraq?

» A plan to transform Iraq from a barren land to green with 5 million trees

» The Housing Fund announces the acceptance of more than 11 thousand loans through the Ur platform

» The Bank of Baghdad is moving to increase its capital to 400 billion dinars

» The electronic payment system will soon be adopted on Iraqi buses

» “It threatens our interests and destroys our economy.” An Iraqi project “irritates” the Kuwaiti stre

» Warning from the Central Bank about “misuse of electronic payment cards”

» Iraq and the Sultanate of Oman are discussing sending capacities through the Gulf countries

» The fact that a decision was issued to deport Syrian workers from Iraq

» Rice comes first... America exports 10 foodstuffs worth more than 350 million dollars to Iraq

» A sixth licensing round for gas exploration

» Baghdad is preparing to host the 50th session of the Arab Labor Conference

» Scientific symposium on the future vision of the tripartite budget

» Five conversion power stations enter service in Najaf

» Planning: Conduct a population census next November

» Experts: Spreading misleading information harms development and investment

» Economists call for tightening money laundering laws and port controls

» Today's newspapers are interested in Sudanese's visit to Anbar Governorate and preparations for cond

» Iraq and Russia discuss cooperation between the two countries in the field of information and artifi

» With international and Arab participation. Diyala University hosts the International Specialized Sci

» The Basra government discusses with a UN delegation support for owners of qualified companies to est

» Oil stabilizes amid signs of an economic slowdown in America

» More than 11 thousand loans announced by the Housing Fund via the Ur platform

» A parliamentarian talks about the "tsunami of multinational begging" and identifies their crossing p

» Iraq alone possesses 9% of the world's reserves...a magical material to stimulate agriculture and th